080-48574040

080-48574040 0

0

Tip #3: How much should you stretch to buy an apartment? : Know these budgeting guidelines

Every time that we plan on buying a new gadget or a car or house we have seen our human mentality tends to stretch a bit further than necessary and end up getting things we do not need or we end up being too stingy and get sub-par products which later we regret for in either scenario.

So, what is the sweet spot that hits the ball out of the park while you choose your apartment. What is that formula that makes sure that you spent the right amount and gone about your purchase of the apartment without hassle? Well abstract as it is, here I shall be telling you on how to plan and to buy your property and the breakdown of those prices so you do not get carried away until it is too late.

Have you noticed the person who raps at the end of the Mutual Investment Advertisements? it is very similar to the price sheet offered to you by the builder. It will just confuse you at the same time tell the truth to you.

So, coming back to the greed and miser part of our mentality, do not over reach neither play it too stingy. Consider you have an annual income 20 Lacs, then the satisfactory price range of a house loan for you would be around 60 Lacs. Basically, multiplying your CTC per year for 3 years is a good start. If you have multiple sources of income and you are sure of your income to increase you could stretch a bit. If you plan on expanding your family it would only make sense to buy a bigger place right now than fall under the stress of having to move to a new place all over again.

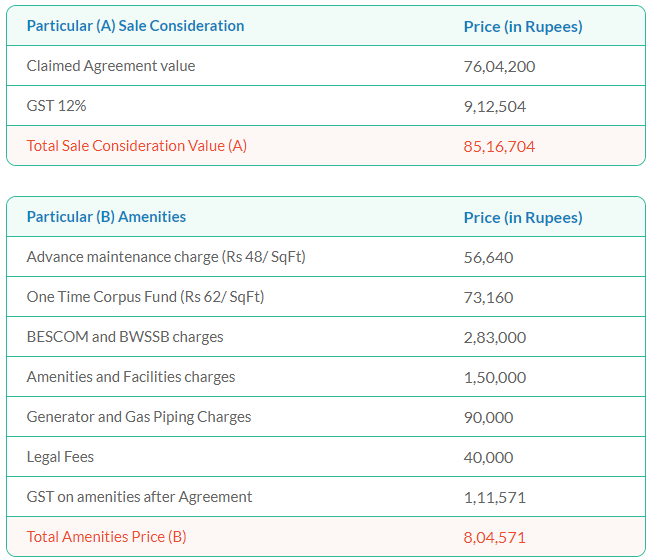

To bring things into perspective lets break down all the charges that the builder has over the base price and acts like its marginal compared to the base price. But reality is the following charges added will massively shift the price and it will overwhelm you. For example, we have taken a price sheet of a reputed builder to show the break up

So, by the breakup it is pretty apparent what the claimed price and what your actual investment will turn up to. Thought the Base rate is the skeletal platform on which the prices are constructed around you will still end up paying a very big and significant amount over that.

Bear in mind the GST is applicable only on properties which do not have an OC, or in other words an under-construction property. Once the OC is delivered the GST is knocked off, but the property value increases significantly adding balance between the post and pre-OC customers, so there is no actual basing on which this is done, this is just a bet the builders take to make sure they keep either side of the bridge happy.

Basically, if a property comes up to one crore finally, the sheer taxes you have paid will fall in the range of 17-18 lakhs on that (i.e, is including the registration) this amount is something you will not be able to fetch back if you sell the property immediately in the near future and plan to make a quick buck. The biggest competitor you will have is the builder themselves because they need a good few years to completely sell the property. To earn a buck over the actual price you paid for the property will take a few years. No short cuts, not even in realty.

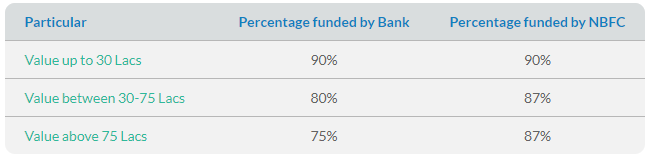

And speaking of money we come to the big brother, the establishment that fund your dreams. The banks. Basically, a bank will be funding ball park around 80% of your property value. This would constitute you to come up with the remaining 20% of the amount by yourself firsthand then the bank shall honor its obligation of the later payment. Also, you are required to have 6.6 % of the total sale value as registration charges and this shall not be fulfilled by the bank. In some cases, even the GST is not fulfilled by the bank. Fundamentally this is variable and is different from bank to bank and their view on the particular builder.

Amount Released On The Total Sale Consideration.

Also, one cannot live in an empty house, can they? It is estimated decent interiors will cost at least 8% to 10% of the sale value. We can surely go for cheaper alternatives, but that will just ruin your wallet in years to come on additional maintenance. Also, some of the fixtures in terms of interior you will not be able to take to your next residence and neither does it appreciate in value when you sell.

Remember to stretch only as much as your bed permits, not overstretch. At the same time the bed should be comfortable too. Research, Patience and Actualization goes a far way. Always remember Zippservian's, be Pragmatic now than be traumatic later.

![]()